We will look at developing a comprehensive strategy that includes designing, executing, measuring, reporting, and monitoring sustainability goals.

The previous article covered how an organisation can design and set Sustainability goals to achieve net zero. We covered topics like setting the organisation’s purpose and values, redesigning the business model based on the objectives set, benchmarking the organisation based on frameworks like the Dow Jones Sustainability Index (DJSI), and understanding the difference between standards, frameworks, and protocols to set short-term and long-term net zero and Environmental, Social, and governance (ESG) targets.

Measurement and Analysis

GHG Accounting

As stated in the preceding article, the GHG Protocol spanning scopes 1, 2, and 3 might be used to account for GHG emissions.

The scope 3 emissions covered under the GHG protocol include the following: Purchased goods and services, Capital goods, Fuel- and energy-related activities, Upstream transportation and distribution (of raw materials/ products the company purchases from vendors), Waste generated in operations, Business travel, Employee commuting, Upstream leased assets, Downstream transportation and distribution (of products the company sells), Processing of sold products, Use of sold products, End-of-life treatment of sold products, and Investments.

Value-chain assessments for greenhouse gas (GHG) emissions are done at the enterprise level (Organisational Life Cycle Analysis/ O-LCA), at a product level (P-LCA), or at a social level (S-LCA), which is not yet mainstream.

We will cover a comprehensive tutorial on GHG Accounting in a future article.

Risk Analysis & Scenario Planning

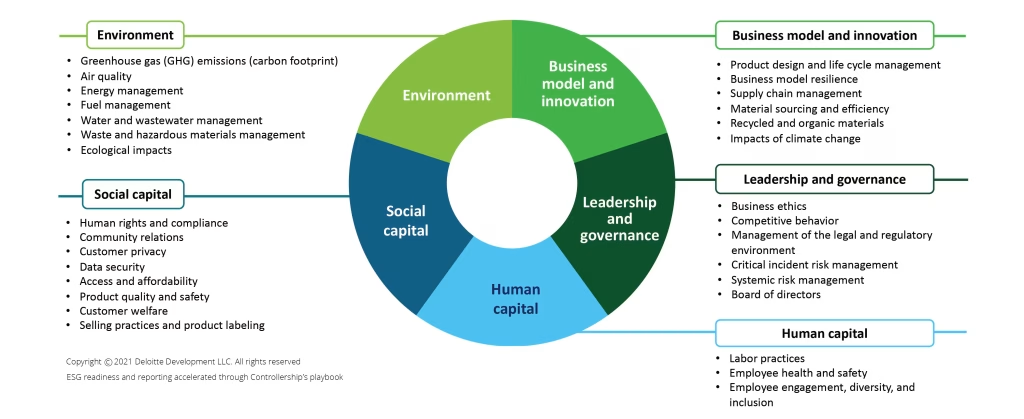

Based on single and double materiality topics (explained in the previous article), organisations usually do environmental, social, financial, and climate modelling at this stage for risk management and, consequently, adhere to compliance. More world governments are urging companies to look at double materiality, where companies place as much importance on how they affect the environment and communities as on how the environment affects their business and revenues. Check out Sustainability Accounting Standards Board’s (SASB) Materiality Finder template for various industries.

Scenario planning is a plan of action for organisations to prepare for uncertain future events. It entails weighing several possible outcomes and determining how to respond to them.

A company can do Socio-ecological modelling through impact assessments to understand how its operations affect the surrounding environment and associated communities positively and negatively since the organisation has socioeconomic impacts on the latter. The four types of impact assessments are social impact assessment, health impact assessment, economic impact assessment and ecological impact assessment. Some frameworks used are Social Return on Investment (SROI) and Principles for Responsible Investing (PRI).

Impact Assessment is not to be confused with Business Impact Analysis (BIA). BIA tells you what to expect when your firm is disrupted (like during black swan events), allowing you to plan ahead of time for recovery, which falls under risk assessment and management (single materiality).

We look at physical and transitional climate risks in climate modelling:

Physical risks involve extreme weather events or long-term shifts in weather patterns and climate change that have the potential to damage or destroy physical assets. Chronic physical risks are long-term shifts in weather patterns (droughts, heat stress, sea level rise), and acute physical risks are increases in extreme weather events (hurricanes, wildfires, floods). The potential impacts include higher costs and reduced revenues due to disruptions in the supply chain, operations, production, and workforce, changes in raw material pricing, and rising insurance premiums.

Transitional climate risks involve business risks associated with transitioning from fossil fuels to a low-carbon economy. These risks include policy and legal (reporting obligations, more exposure to litigation, paying a price for GHG emissions), technology (deploying products with lower emissions or getting subjected to failed investments in new tech), market (increasing raw material cost or change in consumer behaviour), or reputation (stakeholder satisfaction, changes in consumer preferences). The potential impacts of such risks include high insurance premiums, high fines and penalties, costs of compliances and assessments, costs involved in adopting new practices or products or investing in new tech that could be a hit or a miss, as well as high raw material costs and production costs, as well as workforce management and planning (like employee attraction and retention) as well as customer attraction and retention.

Reporting, Disclosures, Key Performance Indicators & Metrics

Sustainability reporting (non-financial reporting) releases information about a company’s ESG performance alongside standard financial measures. This dual approach enables businesses to meet changing regulatory requirements and stakeholder expectations. While there is increasing legal pressure to measure and disclose information to mitigate financial risks due to climate change, there are revenue upsides to disclosing information, like cost optimisation in operations and good access to impact capital.

Once the organisations set and publicly disclose their short-term (to be met by 2030) and long-term (to be met by 20250) targets, they are mandated to report their performance year on year against the metrics or the KPIs they have set.

Just so you know, organisations must first assess their baseline emissions/issues. They must then submit their letter of intent to set short-term and long-term goals. Once the SBTI approves those goals, the annual mandatory disclosures begin.

The Securities and Exchange Board of India (SEBI) requires the top 1,000 listed firms to publish required ESG disclosures in India. These disclosures are given in the annual Business Responsibility and Sustainability Report (BRSR).

The European Union has launched the Corporate Sustainability Reporting Directive (CSDR), and large enterprises already subject to the Non-Financial Reporting Directive (NFRD) are required to comply with new governance standards – European Sustainability Reporting Standards (ESRS)—from January 1, 2025. Non-EU parent companies with large subsidiaries or more than 150 million euros in turnovers must comply. Listed small and medium-sized firms (SMEs) must comply beginning January 1, 2026, while non-listed SMEs may participate voluntarily.

Choosing which framework to use for sustainability reporting is up to the company. While frameworks like the Global Reporting Initiative (GRI) are appropriate for comprehensive ESG reporting, a company can publish a report about climate-related risks using International Financial Reporting Standards S2 (IFRS S2).

In the following article, we will look at ESG implementation, which includes a sustainable transition strategy, a decarbonisation strategy, and monitoring strategies.

Credits

The article is written by Deepa Sai, the founder of ecoHQ.

[…] second article discussed how the organisation can execute Greenhouse Gas (GHG) accounting and conduct risk […]

[…] second article discussed how the organisation can execute Greenhouse Gas (GHG) accounting and conduct risk […]

[…] Greenhouse Gas (GHG) accounting, Risk Analysis, Scenario Planning as well as Reporting and Disclosures – Part 2 […]

[…] GHG accounting, Risk Analysis, Scenario Planning as well as Reporting and Disclosures […]

[…] 5: Beyond GreenwashingPart 4: Inclusive TransitionsPart 3: Materiality, Metrics & JusticePart 2: ESG & Power StructuresPart 1: Systems-Led […]

[…] Greenhouse Gas (GHG) accounting, Risk Analysis, Scenario Planning as well as Reporting and Disclosures – Part 2 […]